Table of Contents

Updated on 11/18/2025

When Is My First Mortgage Payment Due?

As a new homeowner, you’re likely over the moon about closing escrow. Wave goodbye to endless Docusigns, repetitive email chains, and most of all, the lingering fear of not making it to the finish line. Instead, say hello to homeownership!

If you’re someone like me who tends to think one step ahead of the game, you might be wondering the well-known question for homeowners who are fresh out the gate: “When is my first mortgage payment due?”

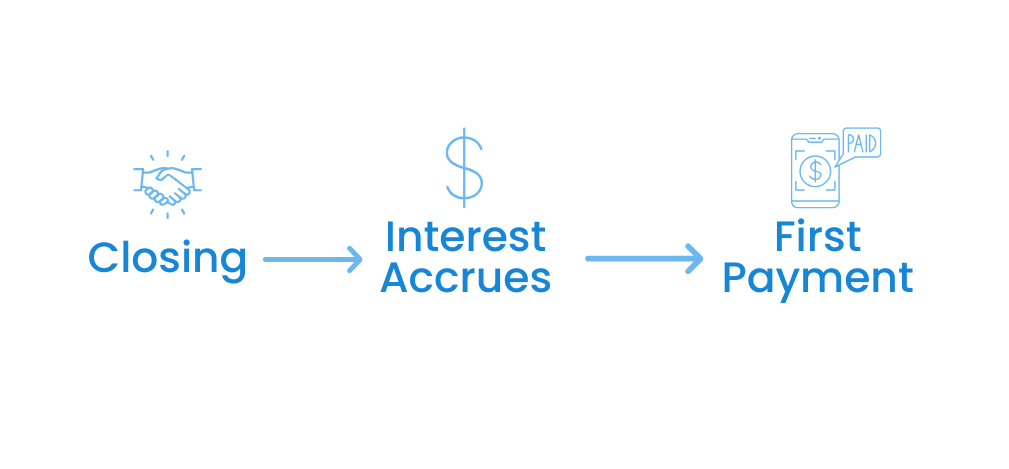

The Short Answer: Not Right Away

If you’re scrambling to pay your first mortgage right after closing, you can relax. Your first mortgage payment is likely due on the first of the month, but not immediately. It’s due at the beginning of the first full month after your closing date. For example, if you closed July 4, your first payment is due September 1. Exact dates vary by lender, closing, and prepaid interest. Always confirm with your loan officer which date to pay.

Before you relax too much, keep in mind that everything happens for a reason. Your mortgage lender isn’t just cutting you slack and giving you a lenient amount of time to pay (although that would be nice). We’ll explain later in the next section what’s happening to your mortgage after you close escrow.

If you close earlier in the month, you’ll likely have a longer timeframe to prepare your financial situation for when your due date draws near.

If you’re still hesitant about the due date, we understand. It can be a strange process that you want to make sure you’re going about as prepared and organized as possible. Here are a few other options to confirm your due date:

- Check your closing documents: You can locate the due date for your first mortgage payment from the package of documents you received at closing. Look for a letter that tells you when your due date is and contains all the details you need to make a payment.

- Ask your loan officer: Your loan officer will know best when your first payment is due. After all, they should be your go-to expert for all questions loan-related! If you have a reliable mortgage lender, don’t hesitate to pick up the phone or send a brief email to put your mind at ease.

Why Is My First Mortgage Payment Not Due Right Away?

Knowing why you don’t pay your mortgage right away will be useful knowledge to take with you if you ever plan on buying another house in the future.

Remember how I said that if you close earlier in the month, you’ll have a longer time before your first payment is due? That period in between is when the interest starts to accrue on your mortgage. These interest costs will be prepaid by you at closing and will vary based on if you scheduled your closing earlier or later in the month.

Going back to my earlier example: If you closed on July 4, you would need to prepay 27 days of interest. On the other hand, if you closed on July 24, you would have to prepay only 7 days of interest.

If you’re still at the stage in escrow where you have time to schedule your closing date, you now have additional information that could sway your decision. Do you want to pay more or less in prepaid interest? Or does the amount of time before your first payment due matter more? Either way, there will be some benefit to whatever you choose.

Is Paying Off Your Mortgage the Same as Paying Rent?

Becoming a new homeowner means you probably upgraded from being the opposite: a renter. Though it is entirely different in aspects such as how much of your equity is increasing, who owns the property, and the longevity of your stay, isn’t it somewhat similar in terms of paying a dollar amount every month?

In a way, yes. Whether renting or having a mortgage, you pay another party monthly as listed in an agreement. Most leases set rent due on the first of each month, similar to mortgage lenders or banks. While some landlords are lenient on late payments, that’s not always true. Surprisingly, a “grace period” is common with mortgage payments and can be less strict than with rent.

Mortgage Payment Methods

Out of the many ways to pay off your monthly mortgage payment, it all comes down to your mortgage lender and what services they offer to streamline the process.

Write a Check

If your mortgage lender is local and family-owned, they might have a traditional way of doing business and request that you mail in a check every month for your payment. This classic method has been used in the industry frequently and is ideal for those that don’t have convenient access to a computer or another mobile device.

Pay Online

Your mortgage lender may allow you to pay through their website or a servicer. As we enter a hyper-digital stage, this is the most common method used by most homeowners and allows for a quick and easy payment process, with only the click of a few buttons.

Paying online also opens up other benefits such as making biweekly payments toward your principal to pay off your house sooner. If you have the extra cash, this could be a plausible consideration. As always, consult with your loan officer first.

Auto-Pay

Setting up auto-pay is not only one of the most convenient transaction methods, it is also a privilege. Not many homeowners have the financial capacity to set up auto-pay, which is completely normal. However, if your cash flow is positive and stable, talk with your mortgage lender about getting this setup.

If you set it up correctly, you’ll rarely miss deadlines, if ever. A great way to confirm that your payment went through is by setting up an alert to your email, so you’re notified of any irregular changes. As a good practice, you should frequently monitor your account to ensure everything is working properly.

Mobile Payments & Digital Wallet

Mobile payments make it easier than ever to manage your mortgage from your phone (APPsolute, 2025). Many lenders offer secure payment options through mobile apps or digital wallets, so you can send or schedule payments anytime. You can also set up automatic drafts or reminders to help you stay on track and avoid late fees.

Is There a “Grace Period” for Late Payments?

Luckily, yes. Without control, we may stumble upon other expenses that were at the time a higher priority than paying our monthly mortgage.

Many lenders offer a grace period of up to 15 days, though this can vary. Be sure to check your loan documents for the exact terms and any late fees that may apply after the grace period ends (Experian, 2023).

Still, you should proceed with caution. Most homeowners should have any kind of bank account, and be fully aware of the fact that transactions don’t go through immediately or even the next day. If you are planning to make a late payment, aim to make the transfer no later than the 10th of the month, allowing up to five days for it to populate in your mortgage account.

You’re All Set!

Our team of experienced loan officers is here to guide you through every step of the homeownership journey with clear communication and expert support. Learn more about setting up your online payments and how to set up autopay with our loan servicing. Whether you’re just starting your homebuying journey or managing your current loan, we are here to provide the guidance and tools you need.